Personal Loans

With a personal loan, you can quickly have cash in hand to pay for things like home improvements, debt consolidation, large purchases and more. Getting approved for a personal loan, however, comes with its own challenges; first, you’ll have to demonstrate to lenders that you have the ability to repay the loan in full and on time.

How can you show lenders that you’re a good candidate for a loan?

Because your credit score is essentially a measure of how likely you are to repay debt, it’s the primary factor lenders will consider to determine your eligibility for their products.

Minimum credit scores required for loans vary depending on the lender you work with, but generally, your credit score will need to be in the 550 – 600 range to be considered for a loan. If your credit score is in this range your lending options will likely be quite limited, and you can expect your loan to come with high-interest rates.

To be considered for a loan with competitive interest rates, you’ll want your score to be somewhere between the 620 – 700 range, but the higher that 3-digit number is, the better. A high credit score increases the likelihood that you’ll be approved for a loan and receive low-interest rates along with it.

If you’re trying to improve your score before applying for a personal loan, keep reading – we’re going to share 5 tips you can use to increase your credit score.

How to Improve Your Credit Score

Pay down credit card debt

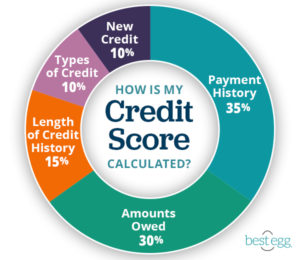

Paying down credit card debt is a crucial step in raising your credit score, especially if you’re carrying large balances on your cards. Why? It all comes down to your credit utilization ratio, the measure of how much credit you’re using compared to how much lenders have extended to you. This factor alone determines 30% of your credit score, so you want to pay close attention to your utilization if you’re looking to improve your score.

Finding your credit utilization ratio is simple: all you have to do is divide your credit card balances by your total credit limit. For example, if you had one credit card with a credit limit of $4000 and the balance on the card was $1000, you’d only be using 25% of your available credit.

FICO recommends using less than 30% of your total credit limit to improve your credit score, but the lower you can keep the percentage, the better. A low credit utilization ratio shows lenders that you only need to use a small amount of the credit that’s been loaned to you, so they may be more confident that you’ll be able to repay a loan on time. The opposite is true if you have a high credit utilization ratio, as high balances on credit cards could indicate to lenders that you’re overextended and may have trouble paying back the loan.

Avoid opening multiple new accounts around the same time

When calculating your score, FICO will look at any new credit inquiries you’ve made or new debts you’ve taken on in the last 6 to 12 months. While taking on new credit doesn’t play a major role in determining your credit score (only 10%), FICO considers borrowers who open multiple new accounts within a short timeframe to be riskier, and as a result, decreases their credit scores. Even opening one new account could hurt your credit score temporarily, but as long as you use the new credit responsibly, your score should bounce back quickly.

New credit can be harmful to your credit score for another reason as well – its impact on the length of your credit history, which determines 15% of your overall score. A component of the above-mentioned credit score factor is the average age of your credit accounts; opening multiple new accounts can drive this average down, which could lead to a decrease in your credit score.

Pay your bills on time

Your payment history determines 35% of your credit score, so making regular on-time payments is critical to improving your score. Depending on the length of your credit history and the number of items affecting your score, even one on-time payment could increase your credit score slightly; with that said, you’ll have to make consistent on-time payments to see a significant improvement.

Pro-tip: A recent FICO study found that a single 30-day late payment can drop a good credit score by 90 – 100 points, even if the borrower has never missed a payment before. If remembering payment due dates is a challenge for you, consider adding reminders to your calendar or setting up automatic bill payments with your lender so you don’t have to face this serious consequence.

Keep unused credit card accounts open

While it may sound illogical, closing credit card accounts that you’re no longer using can harm your credit score. This could happen for two reasons: closing a card can cause your credit utilization ratio to increase and the average age of your credit accounts to decrease. While we briefly touched on these factors in the first and second tips we reviewed, let’s take some time to unpack this.

Increasing your credit utilization ratio: You have 4 credit cards, each of which have credit limits of $2,500, making your overall credit limit $10,000. One of those cards is maxed out at $2,500 and the rest have no balances, so your credit utilization ratio is 25%; a bit high, but still within a healthy range.

If you close one of your unused cards, your overall credit limit will be $7,500, and the $2,500 balance now makes up 33% of your available credit. Now you’re getting into territory that can negatively impact your credit score.

Decreasing the average age of your credit accounts: You have 3 open credit accounts – one is 3 years old, another is 4 years old, and the last is 8 years old. To find the average age of your accounts, you’ll have to add all of the ages up and divide by the total number of accounts; in this case, the average age of your credit accounts would be 5 years old.

If you decide to close the oldest account, the average age of your accounts then becomes 3.5 years old. This decrease in average age can lead to a decrease in your credit score.

Monitor the activity on your credit reports

All three of the major credit bureaus (Experian, Equifax, and TransUnion) offer free credit reports annually. Inaccuracies on your credit report can decrease your score significantly, so it’s worth taking advantage of these free offers to verify that everything looks correct. If you do find any incorrect information on your report, it’s important that you reach out to the bureau(s) as soon as you can to get it corrected.

Pro-tip: Rather than checking your free credit report for each bureau at the same time each year, request your report from a different bureau every four months. This way you can view your free reports throughout the year and have an opportunity to dispute any inaccuracies you find before they become bigger issues.

We briefly touched on a few of the common components of a typical credit score in these tips, but if you want to know all of the factors that could influence your score, you’ll find them (and the level of influence they have on your score) in the graphic below.

To learn about each of the individual factors that influence your credit score in detail, take a look here.

Finding the Right Personal Loan for You (And Your Credit Score)

Finding the right personal loan takes time and careful consideration. In addition to the comparing APR, loan terms and fees, be sure to think about the following:

- What are you planning to use the money for?

- How much will you need?

- Will the payments be affordable?

- How reputable is the lender?

- What’s the minimum credit score to qualify for a loan with the lender?

A Best Egg personal loan could be a good fit for you if you have several years of credit history, the ability to repay the loan and a credit score of 640 or higher. To see if you qualify for a Best Egg loan, visit our personal loans page.

This article is for educational purposes only and is not intended to provide financial, tax or legal advice. You should consult a professional for specific advice. Best Egg is not responsible for the information contained in third-party sites cited or hyperlinked in this article. Best Egg is not responsible for, and does not provide or endorse third party products, services or other third-party content.